Irc 1031 Tax Free Exchange

What Is A 1031 Exchange Commercial Real Estate Md Va Dc

What Is A 1031 Exchange Asset Preservation Inc

1031 Exchange Rules Taking Advantage Of A 1031 Exchange In 2020 1031 Exchange Rules Squar Milner

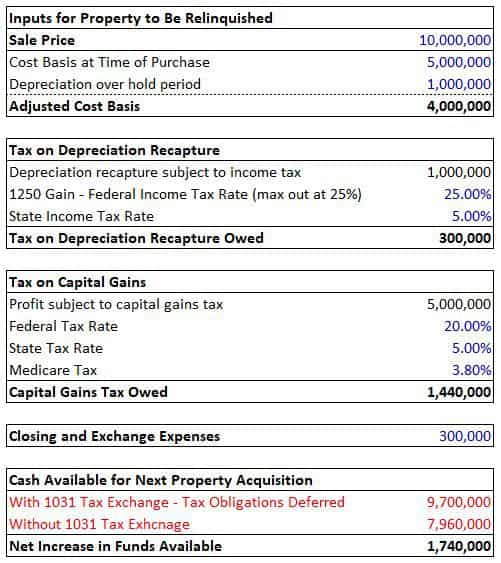

1031 Exchanges By The Numbers Attorneys Cook Cook Commercial Real Estate Investing Exchange Financial Analysis

What S A 1031 Exchange And Why Does It Benefit Investors Nestiny Selling A Business Investing

Image Result For 1031 Exchange Ad Capital Gains Tax Things To Sell Investing

Irc section 1031 provides an exception and allows you to postpone paying tax on the gain if you reinvest the proceeds in similar property as part of a qualifying like kind exchange.

Irc 1031 tax free exchange.

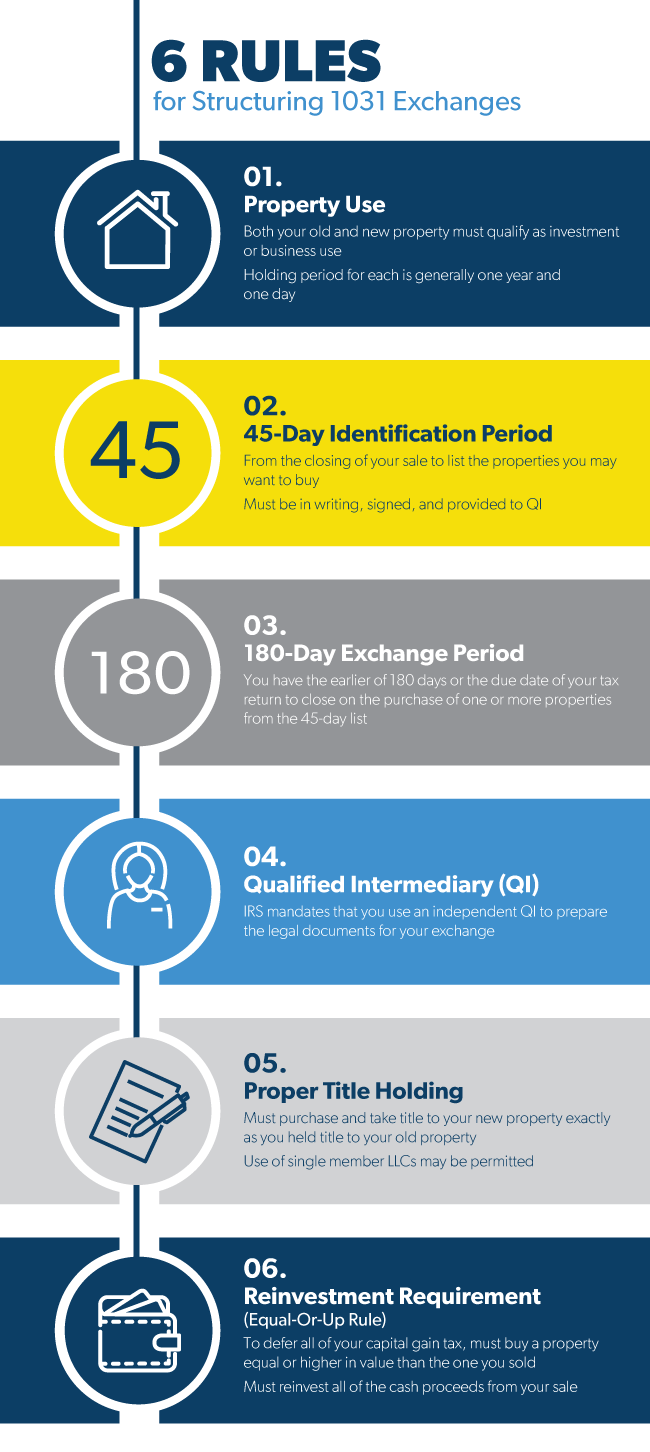

1031 Exchange Rules How To Do A 1031 Exchange

Replacing Debt In A 1031 Exchange Ipx1031

How To Do A 1031 Exchange Rules Definitions For Investors 2020

1031 Exchange Introduction Overview And Analysis Tool Adventures In Cre

How To Do A 1031 Exchange In Nyc Hauseit New York City

Key Considerations In 1031 Exchanges With A Qualified Intermediary First American Exchange Company Exchange Consideration Company

Whats Is A 1031 Exchange Ash Mcginty Co

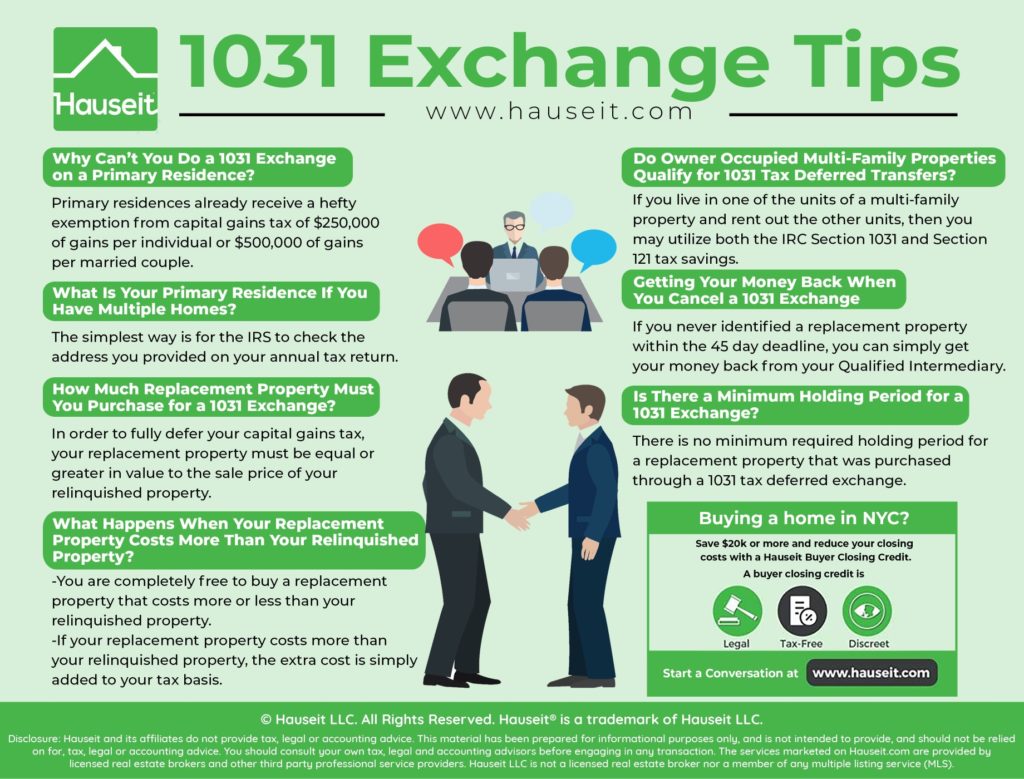

Rules For Converting Rental Property Into A Primary Residence Including After A 1031 Exchange And Claiming The Irc Section Rental Property Rental Residences

1031 Exchange And Primary Residence Asset Preservation Inc

All About 1031 Exchange Other Pins About This Also Real Estate Agent Florida Real Estate Realty

Pin On Benefit Of Irs Section 1031 Exchanges

Eight 1031 Exchange Rules You Can T Ignore Realtor Magazine Ignore Exchange Rules

How To Find The Right 1031 Exchange Property In 2020 Residential Real Estate Real Estate Investing Property

Frequently Asked Questions Faqs About 1031 Exchanges

Capital Gains Tax Calculator Real Estate 1031 Exchange Real Estate Investing Rental Property Investment Property Capital Gains Tax

If You Are Investing Or Thinking About Investing In Real Estate Then You Ll Be Interested In Understanding Th Investment Tools Real Estate Investing Investing

How Is A 1031 Exchange Used In Real Estate

All About 1031 Tax Deferred Exchanges Real Estate Investment Tips Youtube

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcslor5phqfq4gsovpw Rnezlnjf8mckmftqywhelivn0nh6ju K Usqp Cau

What Is Cash Boot In A 1031 Exchange Exchange Authority Llc

How A Dst Works For A 1031 Exchange Investing Mentor Coach Exchange

1031 Investment Exchange Opportunities 1031 Investments Investment Quotes Stock Market Quotes Finance Investing

Home Legal 1031

1031 Exchange The Basics Land Title Association Of Mississippi

An Introduction To The Benefits Of 1031 Tax Deferred Exchanges 1031 Exchange Place

Value Investing Is Risk Aversion Seth Klarman Value Investing Risk Aversion Investing

7 Steps For A Successful 1031 Tax Deferred Exchange By Wendy Patton Http Www Reiclub Com Articles 7 S Real Estate Investor House Rental Real Estate Investing

1031 Exchange Estate Planning Commercial Real Estate Florida Real Estate

1031 Exchange In Colorado The Authoritative Guide To Rules Exchange Companies Requirements And More Inside The 1031 Exchange

Coronavirus 2020 Exchange Extension 1031x Com 1031 Exchange Company

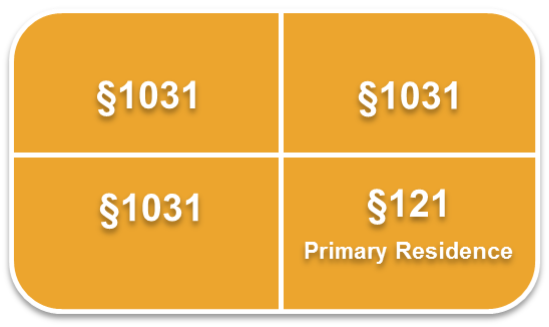

Sections 121 1031 1033 What Is Your Sale 1031 Exchange Experts Equity Advantage

Advanced 1031 Exchanges What Can Be Exchanged 1031 Exchange Experts Equity Advantage

1031 Exchange Property Identification Rules 1031gateway Investment Quotes Sherlock Holmes Finance

1031 Exchange Rule

What Are 501 C 3 Non Profit Organization Https Www Irstaxapp Com What Are 501 C 3 Non Profit Organ Nonprofit Organization Non Profit Internal Revenue Code

Profit On Rental Properties Rental Property Real Estate Investing Rental Property Rental Property Investment

1031 Exchange Into A Reit Reit Exchange Mentor Coach

How To Find The Right 1031 Exchange Property In 2020 Residential Real Estate Real Estate Investing Property

1031 Exchanges Save On Capital Gains Tax But How Do They Work Hoboken Nj Patch

1031 Exchange Two Year Tax Deadline

Account Suspended Business Tax Small Business Tax Tax Help

1031 Exchange Basics 1031 Exchange Basics The 1031 Exchange Is Commonly Used Commercial Real Estate Broker Affordable Life Insurance Commercial Real Estate

1031 Exchange Invest In Boston Real Estate For Your Exchange

1

Source : pinterest.com